|

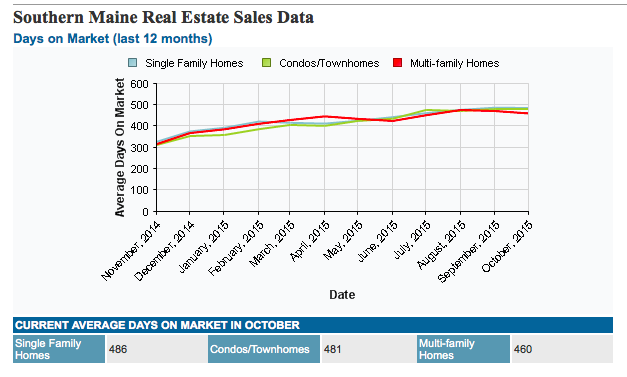

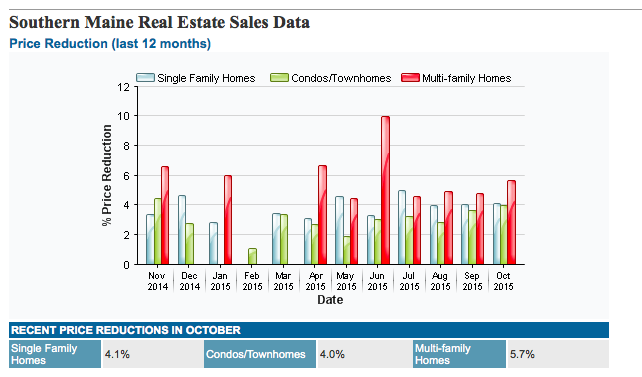

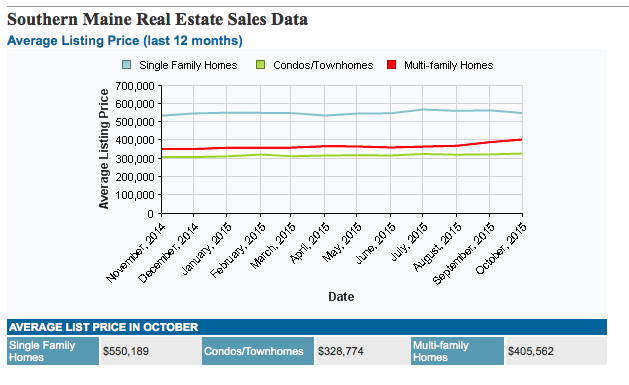

As a real estate professional, I strive to keep in touch with my clients and provide them with information that I hope they will find useful. This blog is an opportunity to let you know about the state of the market and current trends. It may even touch on ways that you could enhance your home's value. I hope the market data and articles will help you with understanding real estate today and help you with your real estate decisions. If you have any questions, please do not hesitate to contact me. Deb Barouch Average Days on the Market Recent Price Reductions Average Listing Price

0 Comments

Along with Wednesday’s release of the minutes from the Federal Reserve’s FOMC meeting from October 27-28, a string of noteworthy economic indicators and closely watched statements by Fed officials caused Treasury yields and bond prices to fluctuate through the week.

The FOMC minutes showed a clear majority of Fed officials were agreeable to a December rate hike while a dovish minority of FOMC members believed the use of the phrase "next meeting" in the policy statement could have been misinterpreted by financial markets as too strong of a signal for a rate hike. Bond yields rallied early in the week, as the Consumer Price Index (CPI) increased for the first time in three months with a gain of 0.2% in October to match the consensus forecast. An additional 0.2% gain was recorded for the year-over-year headline CPI while the Core CPI reading, which excludes food and energy, was 0.2% higher on the monthly reading and was at 1.9% on the year-over-year reading for October. Housing Starts declined 11% during October to a seasonally adjusted annual rate of 1.06 million units, the lowest level since March. Yet, October Starts remained above one million units for the seventh straight month, the longest consecutive monthly run since 2007. This suggests a sustainable housing market recovery remains intact. Meanwhile, Building Permits, a much more forward-looking metric, increased 4.1% to a 1.150 million unit rate last month, exceeding the consensus forecast of 1.137 million. Single family building permits increased 2.4% in October to their highest level since December 2007. Multi-family building permits increased 6.8%. September’s rate of 1,105,000 permits was revised higher from 1,103,000. Also, the November National Association of Home Builders (NAHB)/Wells Fargo Housing Market Index fell 3 points from an upwardly revised reading of 65 in October to 62. Although the November reading was lower than the consensus forecast of 64.5, the revised October reading was the highest since the end of the housing boom in late 2005. As for mortgages, the Mortgage Bankers Association released their latest Mortgage Application Data for the week ending November 13 showing the overall Market Composite Index increased 6.2%. The Refinance Index increased 2.0% from the prior week, while the seasonally adjusted Purchase Index increased by 12% from a week earlier. Overall, the refinance portion of mortgage activity decreased to 58.6% of total applications from 59.8%. The adjustable-rate mortgage segment of activity decreased to 6.3% of total applications from 6.6% the prior week. The average contract interest rate for 30-year fixed-rate mortgages with conforming loan balance rose from 4.12% to 4.18%, its highest level since July 2015. On Friday, the bond market stalled with the yield curve flattening in anticipation of the Fed raising rates in December. Bond traders believe a rate hike within the current environment of low inflation and weakening commodity prices will push yields in shorter-term treasuries higher relative to longer-term Treasuries. This was evident when the yield gap or spread between the two and ten-year Treasuries and the yield gap between five-year and 30-year Treasuries contracted to their tightest levels since August. For the week, the FNMA 3.5% coupon bond gained 12.5 basis points to end at $103.31 while the 10-year Treasury yield decreased 1.1 basis points to end at 2.26%. Stocks ended the week with the NASDAQ Composite gaining 177.04 points to close at 5,104.92. The Dow Jones Industrial Average added 578.57 points to end at 17,823.81, and the S&P 500 increased 66.13 points to close at 2,089.17. Year to date, and exclusive of any dividends, the NASDAQ Composite has gained 7.23%, the Dow Jones Industrial Average has gained 0.004%, and the S&P 500 has added 1.45%. This past week, the national average 30-year mortgage rate decreased to 4.00% from 4.03% while the 15-year mortgage rate remained unchanged at 3.24%. The 5/1 ARM mortgage rate decreased to 2.97% from 3.00%. FHA 30-year rates remained unchanged at 3.75% while Jumbo 30-year rates decreased to 3.83% from 3.84%.  May you have much to be thankful for this upcoming year,

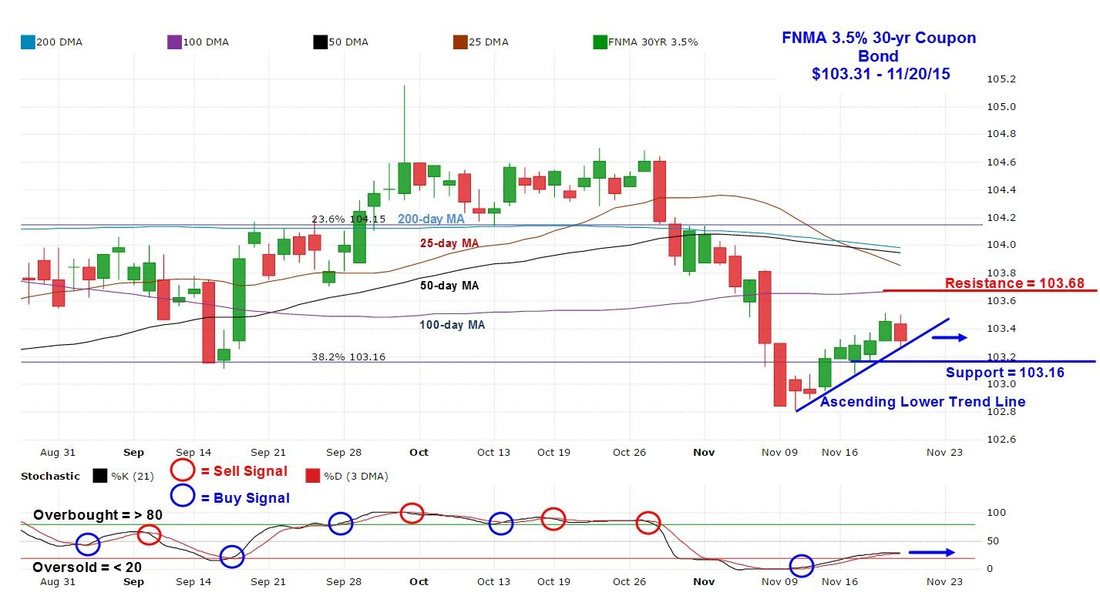

and may your home be filled with wonderful memories this holiday season. For the week, the FNMA 30-year 3.5% coupon bond ($103.31, +12.5 bp) traded within a narrower 44 basis point range between a weekly intraday high of 103.52 and a weekly intraday low of $103.08 before closing at $103.31 on Friday. After trending higher Monday through Thursday, the bond reversed course on Friday in a move toward support located at the 38.2% Fibonacci retracement level at $103.16. Friday’s negative action sent the bond lower to touch its ascending lower trend line. This line is formed by connecting the intra-day lows from the low on November 10 onward to form the lower trend line. A break below this line would be considered a bearish event. The slow stochastic oscillator is showing a loss of momentum and is flattening out, suggesting the bond could subsequently trade sideways and be range-bound between support and resistance located at the 100-day moving average at $103.67. As a result, we shouldn’t see much change in rates this coming Thanksgiving holiday week that will be characterized by lower than average trading volume. Chart: FNMA 30-Year 3.5% Coupon Bond Please enjoy this quick update on what happened this week in the housing and financial markets.

"Thanksgiving is an emotional holiday. People travel thousands of miles to be with people they only see once a year...and then discover once a year is way too often." - Johnny Carson Please note: We will not publish updates next week. Wishing you a wonderful Thanksgiving Day! Rate movements and volatility are based on published, aggregate national averages and measured from the previous to the most recent midweek daily reporting period. These rate trends can differ from our own and are subject to change at any time. 10 SECURITY SOLUTIONS to Keep Your Home Protected

In a book written by Hoover Institute Economist Thomas Sowell some years ago, he traced most of the differentials in housing prices between markets to actions taken by local and state governments. Whether it is through affordable housing actions, impact fees, the setting aside of huge swaths of otherwise developable land, Sowell shows that actions taken by state and local governments profoundly affect the local supply of housing and drive up prices. It’s a good read for those interested.

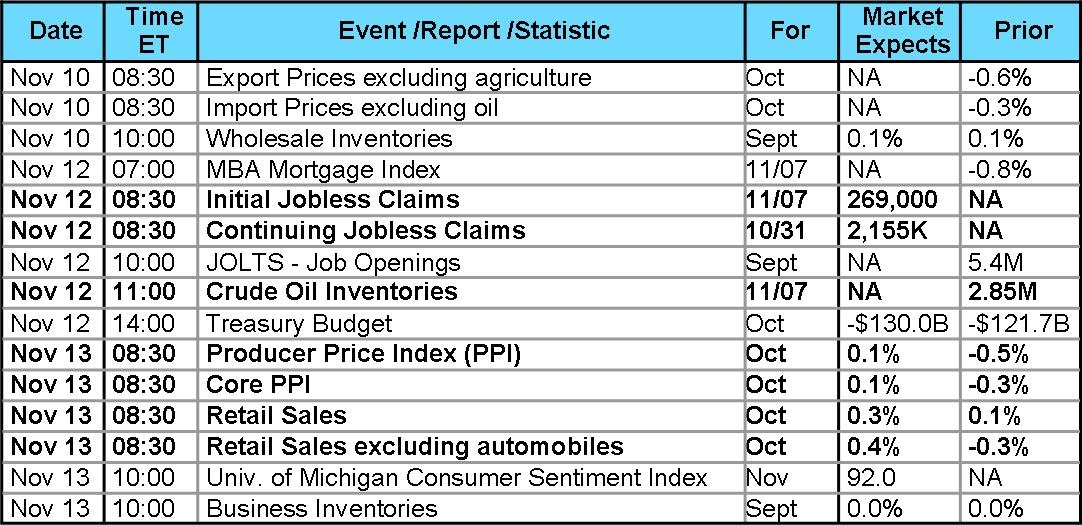

Courtesy of: Tamika Donahue Weekly Review - for the week of November 2, 2015 It was not a good week for the bond market including mortgage bonds. After a slight move lower on Monday, it was all downhill for the bond market with traders exerting caution ahead of Friday’s release of the October Employment Situation Summary (jobs report). The week’s economic news showed the nation’s labor situation seems to be significantly improving. Wednesday’s ADP Employment Change report set the stage for Friday’s jobs data. According to the ADP Employment Change report there were 182,000 private sector jobs added to the economy in October. This jobs total was slightly above the consensus forecast of 180,000 jobs. Also on Wednesday, Federal Reserve Chair Yellen provided a “surprise” to the financial markets during testimony before the House Financial Services Committee, saying the Fed could raise interest rates at its next FOMC meeting on December 16. If so, it would be the first rate hike in almost a decade. Yellen told the Committee "At this point, I see the U.S. economy as performing well. The committee (FOMC) does feel that moving in a timely fashion -- if the data and the outlook justify such a move -- is a prudent thing to do.” Yellen contended that raising interest rates by year end rather than waiting would allow the Fed to gradually raise rates. If the Fed waited too long, it might be forced to raise rates at a quicker pace and that might shock the stock market. Yellen stated "It's been a long time that interest rates have been at zero. Markets and the public should be thinking about the entire path of policy rates over time...that will be a very gradual path." When Friday arrived, both the bond and stock markets were subjected to selling pressure for much of the session following a significantly stronger than forecast October jobs report. The jobs data made it far more likely the Federal Reserve will raise interest rates in December. The U.S. Bureau of Labor Statistics reported total Nonfarm Payroll employment increased by 271,000 in October while the Unemployment Rate was essentially unchanged at 5.0%. This far exceeded the consensus forecast of 181,000 jobs with an unemployment rate of 5.1%. Furthermore, the change in total nonfarm payroll employment for August was revised higher from 136,000 to 153,000, and the change for September was revised lower from 142,000 to 137,000. With these revisions, employment gains in August and September combined were 12,000 more than previously reported. Over the past three months, job gains have averaged 187,000 per month. In housing, the Mortgage Bankers Association released their latest Mortgage Application Data for the week ending October 24 showing the overall Index fell 0.8%. The Refinance Index dropped 1.0% from the prior week, while the seasonally adjusted Purchase Index decreased by 1.0% from a week earlier. Overall, the refinance portion of mortgage activity increased to 59.7% of total applications from 59.5%. The adjustable-rate mortgage segment of activity increased to 6.7% of total applications from 6.6% the prior week. The average contract interest rate for 30-year fixed-rate mortgages with conforming loan balance rose from 3.98% to 4.01%. For the week, the FNMA 3.5% coupon bond lost 81.2 basis points to end at $103.30 while the 10-year Treasury yield increased 17.9 basis points to end at 2.33%. Stocks ended the week with the NASDAQ Composite gaining 93.37 points to close at 5,147.12. The Dow Jones Industrial Average increased 246.79 points to end at 17,910.33, and the S&P 500 added 19.84 points to close at 2,099.20. Year to date, and exclusive of any dividends, the NASDAQ Composite has gained 7.99%, the Dow Jones Industrial Average has added 0.49%, and the S&P 500 has risen 1.92%. This past week, the national average 30-year mortgage rate increased to 4.04% from 3.90% while the 15-year mortgage rate increased to 3.27% from 3.19%. The 5/1 ARM mortgage rate increased to 2.95% from 2.94%. FHA 30-year rates remained unchanged at 3.75% while Jumbo 30-year rates increased to 3.85% from 3.71%. Mortgage Rate Forecast with Chart For the week, the FNMA 30-year 3.5% coupon bond ($103.30, -81.2 bp) traded within a wider 101 basis point range between a weekly intraday high of 104.14 and a weekly intraday low of $103.13 before closing at $103.28 on Friday. Friday, the bond plunged below primary support at the 100-day moving average at $103.66 and secondary support located at the 38.2% Fibonacci retracement level at $103.16 before bouncing back off of its worst levels of the day. The $103.16 level now becomes primary support while the 100-day moving average now becomes nearest overhead resistance. The “slow” stochastic oscillator measuring market momentum has totally flat-lined and can’t move any lower with a current reading of zero. Therefore, any price move higher by mortgage bonds this coming week will trigger a new buy signal. Should this occur, we should see a slight improvement in mortgage rates. Chart: FNMA 30-Year 3.5% Coupon Bond   Economic Calendar - for the Week of November 9, 2015 The economic calendar features the weekly Initial Jobless Claims, Producer Price Index and Retail Sales reports as the most likely to impact the financial markets this coming week. Economic reports having the greatest potential impact on the financial markets are highlighted in bold. Federal Reserve FOMC Meeting Schedule Upcoming Federal Reserve FOMC Meeting Schedule & Rate Hike Probability**

* Meeting associated with a Summary of Economic Projections and a press conference by the Chairman. ** Probability generated from the CME Group FedWatch tool based on the 30-day Fed Funds futures prices. Tamika Donahue Branch Manager, NMLS# 399388 Residential Mortgage Services 24 Christopher Toppi Drive South Portland, ME 04106 (207) 523-8416 (207) 749-4364 [email protected] www.RMSmortgage.com/TamikaDonahue |

Deb BarouchWith over 30 years of experience helping Maine buyers & sellers!  Archives

June 2017

Categories

All

|

RSS Feed

RSS Feed

|

Keller Williams Realty

Greater Portland 50 Sewall Street, 2nd Fl Portland, ME, 04102

|

|

Copyright © 2000-2015 Keller Williams ® Realty. - a real estate franchise company. All information provided is deemed reliable but is not guaranteed and should be independently verified. Properties subject to prior sale or rental. Each brokerage is independently owned and operated.

|

Proudly Designed by: eAgentCreative

|