|

FOCUS ON TRID: Advice from Linda Gifford, Maine Association of Realtors® Legal Counsel

Even if you have bought or sold property in the past, the rules and documentation is changing - As part of the changes, which stem from the merger of the Real Estate Settlement Procedures Act (RESPA) and the Truth in Lending Act (TILA), two new forms—the Loan Estimate and the Closing Disclosure—will replace the HUD-1 settlement form and the Good Faith Estimate. Samples of the new forms are available from the Consumer Financial Protection Bureau. What can you do to smooth out the process for your closing as the buyer or seller? The number one thing buyers and sellers can do is communicate, early and often with your real estate agent and with your lender (both buyers and sellers will be providing info to the buyer's lender or if your are having a cash sale, your title company or attorney). Your real estate agent will be communicating with you about the transaction and keeping you informed as to dates and timelines. Buyers: You should check in with the lenders you tend to use and see what their processes will be. How have they chosen to implement the disclosure process to you (the borrower)? What can you do to help? What does your agent suggest you put in your offer for days to close (we recommend 45-60 days) in your purchase and sale agreement? For more guidance from the CFPB: Click Here Points in the transaction where you can make a difference:

The Deb Barouch Team has extensive knowledge of the industry with over 30 years of experience. We know dependable loan officers, home inspectors, etc to help you through this process. Please contact us if you have any real estate needs! Deb Barouch Broker | Keller Williams Realty O: 207-553-2403 C: 207-838-4875 www.SearchMaineHomes.net www.MaineLuxuryPortfolioHomes.com www.SearchMaineCondos.com www.SearchMaineHomeValues.com

0 Comments

Portland Landlords are required to register all rental units with Portland Housing Safety Office in 2016Beginning January 1, 2016, all Portland rental units MUST be registered annually with the City of Portland Housing Safety Office. The fine for failing to comply is $100 per unit per day.

Here is some information that you will find of interest if you rent out your condo or own an investment property in Portland: The registration form can be downloaded here: http://www.portlandmaine.gov/DocumentCenter/View/11080 The registration cost per unit is $35. There are discounts available for such things as having a fully sprinklered building, centrally monitored fire alarm, various inspections, and a "non-smoking" lease. Units must be registered annually, and within 30 days of purchasing the property. There are fines of up to $100 per day per unit for noncompliance. The rules applies to ALL rentals: Single family, casual rentals, AirBnB, vaction homes, weekend rentals, etc. The City intends to monitor internet advertisements on Craigslist and other sites.  Buyers are finally being able to take advantage of cooling trends in previously hot markets. Multiple offers are no longer being thrown at sellers as soon as the For Sale sign hits the front yard. Here's a tip about negotiating the best deal.

Make sure you look at the big picture. In changing markets you should be planning to stay for at least five years, so don't get caught up in a $2,000 price difference. Remember, the goal is to get the house you want to live in for some time, not to impress friends with how you worked the previous owner. There was a significant amount of economic news released during the Thanksgiving holiday-shortened trading week. Overall, the economic data was strong enough to support the idea the Federal Reserve will likely pull the trigger on the first rate hike in nine years when the next rate decision is released on December 16.

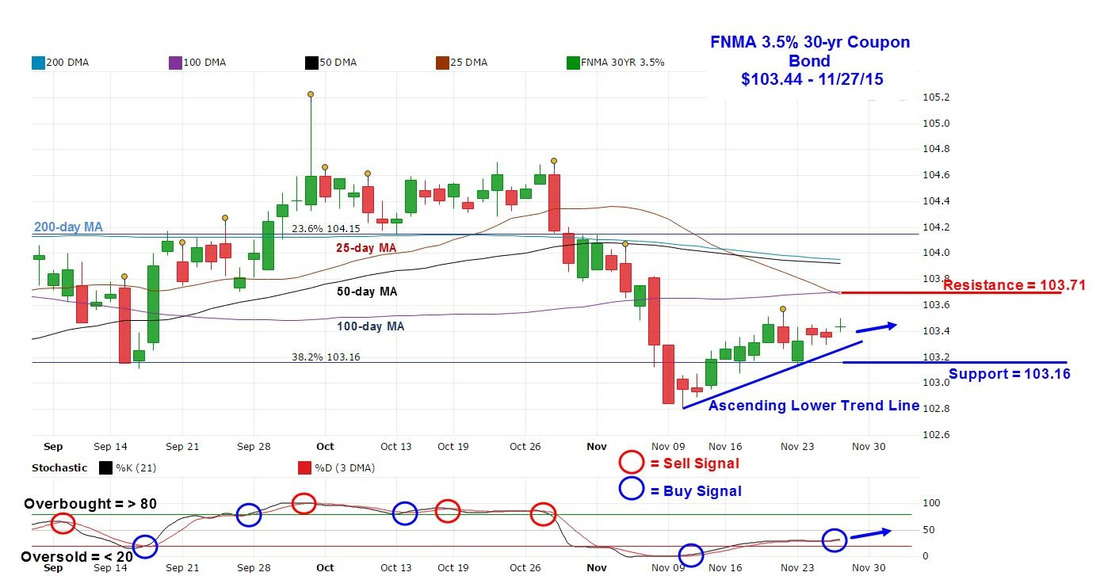

The week began with a report on home sales when the National Association of Realtors (NAR) reported Existing Home Sales declined 3.4% on a sequential basis in October, to a seasonally adjusted annualized rate of 5.36 million homes. However, Existing Sales were still 3.9% above the year-earlier figure. The consensus forecast had called for an annualized sales rate of 5.50 million homes. Overall, the median price of an existing home increased 5.8% to $219,600. NAR chief economist Lawrence Yun remarked “As long as solid job creation continues, a gradual easing of credit standards even with moderately higher mortgage rates should support steady demand and sales continuing to rise above a year ago.” For the week, the FNMA 30-year 3.5% coupon bond ($103.44, +12.5 bp) traded within a narrower 36 basis point range between a weekly intraday high of 103.50 and a weekly intraday low of $103.14 before closing at $103.44 on Friday. As projected last week, the bond traded mostly in a sideways direction between technical support located at the 38.2% Fibonacci retracement level at $103.16 and technical resistance located at the 100-day moving average at $103.71. The ascending lower trend line remains intact while the slow stochastic oscillator indicating market momentum has made a slight positive crossover while remaining far from “overbought” and this is a positive outcome. If the week’s employment data supports a December rate hike by the Federal Reserve we could see mortgage rates improve slightly. Chart: FNMA 30-Year 3.5% Coupon Bond  Courtesy of:

Tamika Donahue Branch Manager, NMLS# 399388 Residential Mortgage Services 24 Christopher Toppi Drive South Portland, ME 04106 (207) 523-8416 (207) 749-4364 Tamika.Donahue@RMSmortgage.com www.RMSmortgage.com/TamikaDonahue  12/4 Village Holidays & Midnight Madness Sale, Bar Harbor

12/5 Rangeley Parade of Trees Community Party 12/6 Santa Sunday at Sunday River 12/6 Christmas Doubles/Lasagna Dinner at Woodland Valley, Limerick 12/6-12 Yarmouth Holiday Craft Show 12/19 Community Free Ski Day, Quarry Road Trails 12/19 Grand Opening Party, Big Squaw Mountain 12/26 Mt. Abram Full Moon Hike & Ski 12/31 New Years Eve at The Birches, Rockwood  Whether you plan to sell in the near future, or just want to improve the value of your home, here is one low cost improvement you should consider.

Replace bathroom fixtures. Bathroom and kitchen fixtures may work fine over a long period of time, but the finish will corrode and lose its shiny coat. So replacing these knobs will naturally give the bathroom or kitchen a more updated look. A quick fixture change, a new toilet seat and fresh accessories can be all you need to brighten up the bathroom.  Fridge or Freezer won't CoolOne common fridge malfunction is the loss of electricity. If the inside light doesn't come on, check the fridge is plugged in and check the breaker panel. If this doesn't help, try these fixes to restore the chill:

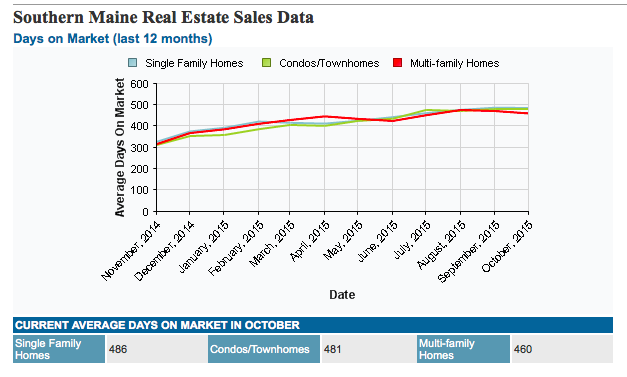

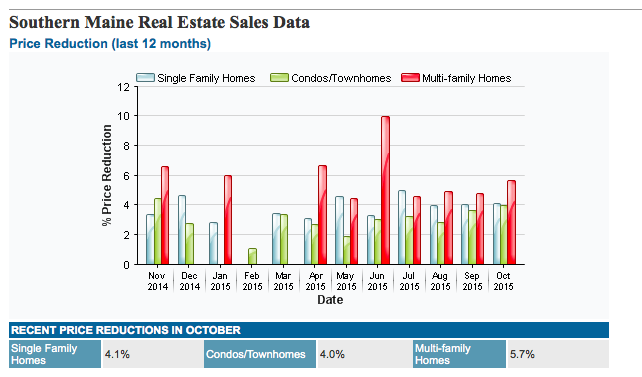

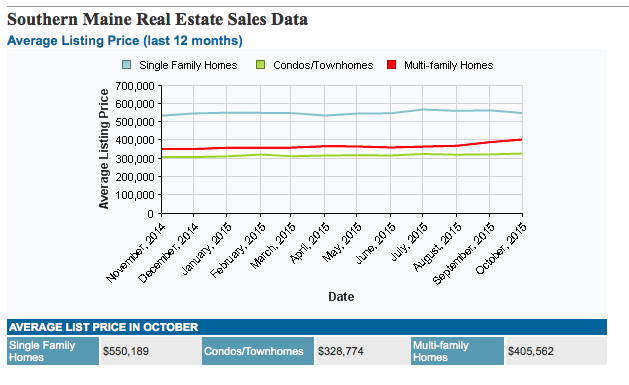

Check thermostat and vents. Has the temperature control dial inside the fridge been turned down? Are the fridge and freezer vents blocked by food containers? Clean the coils. Air must flow freely through the condenser coils to chill the fridge. Generally, these coils are on the back. Items on top of the fridge or stuffed behind it will reduce the airflow. Newer fridges have coils underneath, and may be blocked or plugged with objects or dust. To keep the fridge efficient, pull off the front grille and clean the coils. Do annually, or each 6 months if you have pets. Buy a long brush for $8 for this job. Free up the condenser fan. Coils on the back of a fridge create airflow as they heat up. Models with coils underneath have a fan. Dust buildup can slow the fan; trash can stop it altogether. As a real estate professional, I strive to keep in touch with my clients and provide them with information that I hope they will find useful. This blog is an opportunity to let you know about the state of the market and current trends. It may even touch on ways that you could enhance your home's value. I hope the market data and articles will help you with understanding real estate today and help you with your real estate decisions. If you have any questions, please do not hesitate to contact me. Deb Barouch Average Days on the Market Recent Price Reductions Average Listing Price Along with Wednesday’s release of the minutes from the Federal Reserve’s FOMC meeting from October 27-28, a string of noteworthy economic indicators and closely watched statements by Fed officials caused Treasury yields and bond prices to fluctuate through the week.

The FOMC minutes showed a clear majority of Fed officials were agreeable to a December rate hike while a dovish minority of FOMC members believed the use of the phrase "next meeting" in the policy statement could have been misinterpreted by financial markets as too strong of a signal for a rate hike. Bond yields rallied early in the week, as the Consumer Price Index (CPI) increased for the first time in three months with a gain of 0.2% in October to match the consensus forecast. An additional 0.2% gain was recorded for the year-over-year headline CPI while the Core CPI reading, which excludes food and energy, was 0.2% higher on the monthly reading and was at 1.9% on the year-over-year reading for October. Housing Starts declined 11% during October to a seasonally adjusted annual rate of 1.06 million units, the lowest level since March. Yet, October Starts remained above one million units for the seventh straight month, the longest consecutive monthly run since 2007. This suggests a sustainable housing market recovery remains intact. Meanwhile, Building Permits, a much more forward-looking metric, increased 4.1% to a 1.150 million unit rate last month, exceeding the consensus forecast of 1.137 million. Single family building permits increased 2.4% in October to their highest level since December 2007. Multi-family building permits increased 6.8%. September’s rate of 1,105,000 permits was revised higher from 1,103,000. Also, the November National Association of Home Builders (NAHB)/Wells Fargo Housing Market Index fell 3 points from an upwardly revised reading of 65 in October to 62. Although the November reading was lower than the consensus forecast of 64.5, the revised October reading was the highest since the end of the housing boom in late 2005. As for mortgages, the Mortgage Bankers Association released their latest Mortgage Application Data for the week ending November 13 showing the overall Market Composite Index increased 6.2%. The Refinance Index increased 2.0% from the prior week, while the seasonally adjusted Purchase Index increased by 12% from a week earlier. Overall, the refinance portion of mortgage activity decreased to 58.6% of total applications from 59.8%. The adjustable-rate mortgage segment of activity decreased to 6.3% of total applications from 6.6% the prior week. The average contract interest rate for 30-year fixed-rate mortgages with conforming loan balance rose from 4.12% to 4.18%, its highest level since July 2015. On Friday, the bond market stalled with the yield curve flattening in anticipation of the Fed raising rates in December. Bond traders believe a rate hike within the current environment of low inflation and weakening commodity prices will push yields in shorter-term treasuries higher relative to longer-term Treasuries. This was evident when the yield gap or spread between the two and ten-year Treasuries and the yield gap between five-year and 30-year Treasuries contracted to their tightest levels since August. For the week, the FNMA 3.5% coupon bond gained 12.5 basis points to end at $103.31 while the 10-year Treasury yield decreased 1.1 basis points to end at 2.26%. Stocks ended the week with the NASDAQ Composite gaining 177.04 points to close at 5,104.92. The Dow Jones Industrial Average added 578.57 points to end at 17,823.81, and the S&P 500 increased 66.13 points to close at 2,089.17. Year to date, and exclusive of any dividends, the NASDAQ Composite has gained 7.23%, the Dow Jones Industrial Average has gained 0.004%, and the S&P 500 has added 1.45%. This past week, the national average 30-year mortgage rate decreased to 4.00% from 4.03% while the 15-year mortgage rate remained unchanged at 3.24%. The 5/1 ARM mortgage rate decreased to 2.97% from 3.00%. FHA 30-year rates remained unchanged at 3.75% while Jumbo 30-year rates decreased to 3.83% from 3.84%. |

Deb BarouchWith over 30 years of experience helping Maine buyers & sellers!  Archives

June 2017

Categories

All

|

RSS Feed

RSS Feed

|

Keller Williams Realty

Greater Portland 50 Sewall Street, 2nd Fl Portland, ME, 04102

|

|

Copyright © 2000-2015 Keller Williams ® Realty. - a real estate franchise company. All information provided is deemed reliable but is not guaranteed and should be independently verified. Properties subject to prior sale or rental. Each brokerage is independently owned and operated.

|

Proudly Designed by: eAgentCreative

|